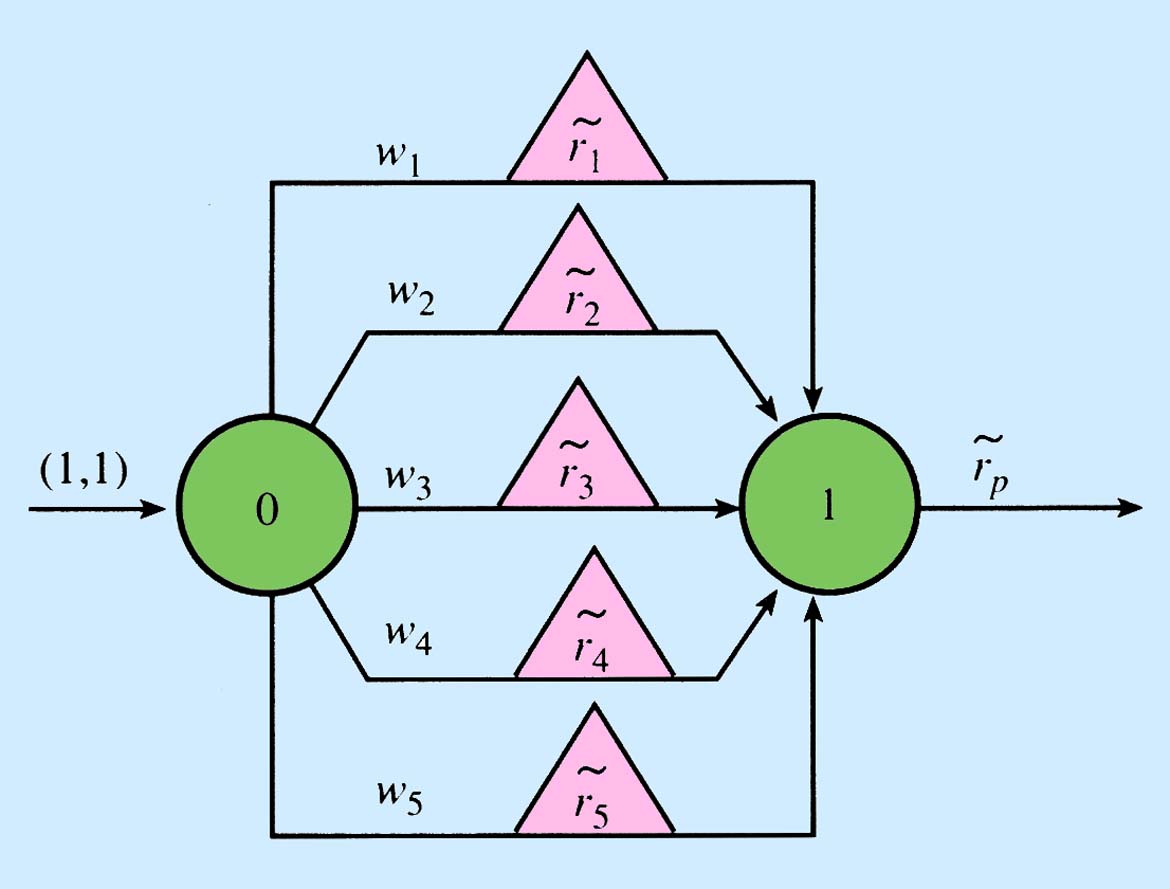

The above figure shows the basic portfolio network for portfolio selection under uncertainty in one period. Now the multipliers or returns on each investment arc are uncertain. The multipliers are being generated by a probability distribution or by a stochastic process. With stochastic multipliers the portfolio network becomes a stochastic […]

Stochastic Portfolio Network for Portfolio Selection under Uncertainty

portfolio network. The optimization problem will be to maximize the flow out of node 1. In order to control the uncertainty generated by the return stochastic process the total variance of the portfolio return can be constrained. Notice that in this portfolio network model the input arc into node 0 is constrained to be 1. This will result in weights that represent the optimal investment percent in each the five investments.

MEAN-REVERSION RISK IN PORTFOLIO MULTIPLIERS

In stochastic portfolio networks we need a model of the uncertainty process that is generating the stochastics multipliers. The modern portfolio theory solution (by Markowitz) was to assume that all return processes are random walks and that the uncertainty in the multipliers or the risk generating the multipliers can be described by normal distributions. The random walk hypothesis was essential since it meant that the multipliers did not need to have any time dependent nature. In a random walk as in modern portfolio theory the return distribution is independent of time. Returns are independent and identically distributed across time. Digital portfolio theory (by Jones) on the other hand, proposes that the returns are being generated by a mean-reverting stochastic process. Returns are not independent and identically disturbed over time. Jones proposed using the digital signal process description of returns. Return can have multiple mean-reverting patterns. These mean-reverting patterns produce more risk at mean-reversion lengths that are institutionally relevant to the return generating process. Different investments are affected differently over different lengths of time. However, most investments are more strongly influenced over time by calendar length mean-reversion periods. The business and market calendar drives the stochastic risk of the financial system. In signal processing we say that calendar frequency is the carrier signal for risk. Go to the Examples page for examples of these risks in different industries.

Phasor Representation of Systematic and Unsystematic Mean-Reversion Risk

The figure above shows the digital portfolio theory description of risk. Now risk is represented by a vector (phasor). A particular mean-reversion length risk will have a vector of risk with both amplitude (standard deviation) and direction (angle relative to the markets risk). Digital portfolio theory allows the risk at a particular frequency to be broken into two components; the systematic risk or beta risk and the unsystematic risk or alpha risk. The sum or these two risks equals the total risk for that particular mean-reversion length.